The holy grail for UK pension schemes? - Investment Consultants and Advisors Newsletter Issue 2

The holy grail for UK pension schemes? - Investment Consultants and Advisors Newsletter Issue 2

The purpose of a pension scheme is to pay out liabilities as they fall due, and to provide members with a secure financial future.

In an ideal world, pension schemes would achieve this by investing a significant proportion of their assets in a low risk matching portfolio.

This would typically contain index-linked gilts and investment grade credit which could be structured to ensure all future liability cashflows would largely be met with the income and redemption proceeds from bonds and credit securities.

The decline in UK government bond yields over the last decade has left many defined benefit schemes with significant funding deficits, and investment grade credit has become increasingly expensive, necessitating that investors cast their nets wider to meet their funding objectives.

Against these economic challenges, the environmental and societal issues facing humanity today have also exacerbated.

As stewards of capital, institutional investors have unrivalled influence in directing capital to investment opportunities that have the potential to deliver positive environmental and social impact.

Gilt substitutes

In the current low-yield environment, pension schemes can no longer afford to invest as much of their portfolio in traditional matching assets.

In order to meet member benefit payments and close funding gaps, the spotlight has moved to substitute strategies that have the potential to provide a return above gilts, whilst also providing secure long term, inflation-linked cashflows.

The industry has dubbed these “secure income assets”.

Secure income is an umbrella term that refers to income-generating investments that offer the potential for attractive liability-matching characteristics, through predictable, resilient, inflation-linked cashflows.

A key feature of secure income assets is that they may offer a return in excess of risk-free government bonds whilst retaining strong long-term matching attributes.

There is no litmus test for whether an asset can be considered ‘secure income’, however.

Cashflows will either be contractual in nature via long-term leases for example, or directly linked to revenues backed by long-term contracts with high-quality counterparties.

In many cases, cashflows will be underpinned by collateral or benefit from other contractual protections.

Another common feature of secure income assets is low economic sensitivity which helps maintain long-term resilience.

The secure income universe encompasses a range of strategies across real estate, infrastructure, renewable energy and real asset debt, but the aim remains the same: to achieve superior risk-adjusted returns above index-linked gilts over time and an attractive cash-flow pick up.

Increasing scarcity

Attractive assets with secure, long-dated inflation-linked income have seen significant demand, not only from domestic pension schemes but from global pension schemes, wealth funds and particularly large insurance companies seeking to match annuity liabilities.

Popular secure income sub-asset classes such as ground rents, senior infrastructure debt and housing association finance have experienced considerable yield compression.

Whilst these sectors remain highly attractive for secure income investing, investors can find greater levels of yield pickup if they cast their net a little wider into specialised sectors.

Investing with purpose

At Gresham House, we pride ourselves on being specialists in alternative investment solutions.

We have the dual objective of helping our clients to access specialist investment opportunities ahead of the crowd, whilst also making a meaningful contribution to advancing the world’s transition to a more sustainable way of life.

Gresham House offers a range of sustainable investment opportunities, providing our clients with solutions in less well-understood areas of the investment universe. This is where we believe superior investment outcomes can be found.

We believe in purposeful investment where investment outcomes and positive environmental and social impact go hand-in-hand.

If investors can combine secure income returns with the opportunity to deliver positive social and environmental impact – could this be the holy grail?

Our core strategies for investors searching for secure income aim to deliver benefits to our people and our planet.

We call them secure income investing with purpose.

Shared ownership housing

Regardless of the economic environment, people need good quality, affordable homes.

In the UK, home ownership is out of reach for all but the highest earners, leaving many middle and lower earners stuck in low quality, privately-rented accommodation, earning too much for social housing and too little to buy and therefore struggling to put down roots.

Shared ownership housing is an ultra-long lease real estate investment strategy, which aims to provide an affordable route to home ownership for low and middle earners.

On average, shared owners will own 30% of the equity in their home, and rent the remaining portion from a registered provider. (gov.uk – Help to Buy; Gresham House analysis 2021)

Unlike typical rental contracts of one to two years, shared ownership leases are ultra-long term (typically 999 years).

It is through this long-term contracted rental income that the strategy delivers secure inflation-linked cashflows to investors.

Shared ownership customers risk voiding their share of their home if rental payments are not made, which creates a strong alignment of interest with investors.

Shared ownership quadruples the number of people who meet the criteria needed access to home ownership. (Gresham House analysis, May 2021)

It does this through lower deposit requirement and discounted rents.

Registered providers of shared ownership can receive a government contribution of c.£30,000 per new shared ownership home making it an even more attractive asset class in which to invest (subject to individual circumstances and as such subject to change).

Unsubsidised renewables and energy storage

The need for increased renewable energy capacity presents a clear investment opportunity (three times existing renewable capacity). (Aurora scenario analysis, based on meeting “net zero” with moderate renewable energy increase)

Subsidy schemes for renewable assets in the UK no longer exist, meaning all new renewable capacity built in the UK will be unsubsidised.

Unsubsidised renewables such as solar and wind assets on the other hand typically offer a 1%+ premium versus subsidised assets. (Past performance is not a reliable indicator of future performance).

The technologies are well established and the availability of long-term fixed price contracts mitigates power price risk and provides cash flow certainty for investors.

Battery energy storage assets are essential to facilitating UK renewable build-out, and further revenue streams can be secured using enhanced Power Purchase Agreement (PPA) strategies through the addition of collocated battery storage assets.

Rather than being an obstacle, the private nature of secure income assets means that many are naturally aligned with ESG objectives by virtue of their purpose and function – from clean energy to social housing.

For these reasons, we believe the time is right for investors to consider allocating to secure income strategies such as those cited above. Investors have the opportunity to capitalise on the energy transition revolution and have the potential for a healthy income at a time when traditional asset classes are falling short.

At Gresham House, we deliver effective and alternative investment solutions to help clients achieve their financial objectives whilst making a meaningful contribution to advancing the world’s transition to a more sustainable way of life.

As the world faces multiple crises – from the pandemic to climate change – we believe that now is the time for us all to commit to responsible investing.

The views expressed here are at the date of publication (January 2022) and as such are subject to change.

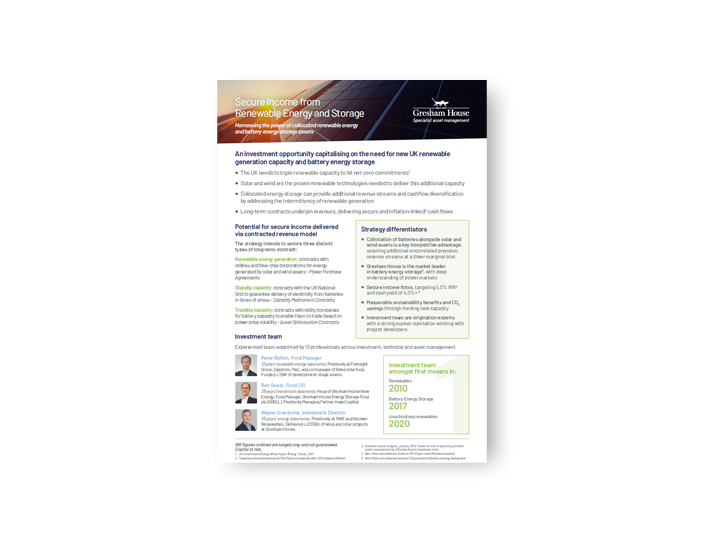

The investment opportunity

Significant investment is needed in new renewable energy assets to meet both net-zero carbon targets and increasing electricity demand.

Battery energy storage assets are crucial in facilitating renewables, helping to assuage power supply-demand imbalances linked to intermittent generation.

The proposed new fund, Secure Income from Renewable Energy & Storage LP, plans to invest in these proven technologies, offering secure income cashflows underpinned with contracted revenues for the first ten years.

Full details, including risk factors, will be detailed in the offering documents.

Differentiators

- Secure income – prioritisation of contracted revenue strategy, unlike many other renewable funds

- Return premium – enhanced returns vs acquiring operating renewable assets, strengthened with cost efficiencies from locating batteries adjacent to renewable generators

- Cashflow diversification – cashflows from battery storage and renewables are inversely correlated

- Tangible ESG benefits – rare opportunity to invest in greenfield assets at scale, delivering ‘additionality’ vs. existing assets

Sustainable investment

|

| Gresham House Sustainable Investment Report

Gresham House released its inaugural Sustainable Investment Report in March 2021. The sustainability industry evolved rapidly during 2020 as demand for investments that meet return objectives whilst benefiting wider society and the environment increased, and this report provides an insight into our progress. |

Director, Sustainable Investment Rebecca Craddock-Taylor discusses the November 2021 COP26 conference, focusing on the change we expect to see as a result of the commitments made.

Rebecca reflects on the conference priorities, whether it achieved what it set out to, and some of the most pertinent outcomes for investors.

How to invest in renewable energy and battery energy storage

For more information, please contact our Consultant Relations team – consultantrelations@greshamhouse.com

|

|

|

| James Lindsay Head of Institutional Business j.lindsay@greshamhouse.com |

Catriona Buckley, CFA Institutional Business Development Director c.buckley@greshamhouse.com |

Keisha-Ann Duodu Institutional Sales Associate k.duodu@greshamhouse.com |