Ken Wotton & Brendan Gulston - June 2020

Ken Wotton & Brendan Gulston - June 2020

Despite sweeping dividend cuts across the UK equity space in the last couple of months, investors should think twice before making rash changes to their portfolios.

The most recent edition of the Link Group UK Dividend Monitor showed that more than 50% of UK dividends for 2020 – representing £50.6bn – have been cut or are at risk of being cut, with just 32% classified as ‘safe’.

Below, managers of the LF Gresham House UK Multi Cap Income Fund, Ken Wotton and Brendan Gulston highlight six rules for income investing in this crisis that they believe investors should consider when choosing an income strategy.

With the majority of total dividends coming from a handful of names in the FTSE 100 index, crowding into those stocks by large-cap focused funds means any cuts will have a disproportionate effect.

As such, we advocate an approach that takes a broader range of stocks into account.

By adopting a broader focus and looking down the market capitalisation spectrum, investors can find smaller businesses dominant in niche areas, which are less susceptible to broad market movements and more insulated from certain global macroeconomic risks.

For example, kettle control manufacturer Strix (dominant position in its market) and online comparison platform Moneysupermarket (cash-generative business with little leverage) have both confirmed dividends more recently.

Sector awareness has become increasingly important during the crisis as different parts of the market have been affected differently.

Financials, for example, have been hardest hit with banks hit by a mandated 12-month halt to shareholder payments by the Bank of England – wiping out £13.6bn of dividends this year.

Shocks have been felt in housebuilding and mining too, while energy giants are also reeling from the fall in oil prices as Royal Dutch Shell cut its dividend for the first time since the second world war.

Cyclicals struggle more in a downturn, therefore avoiding these businesses and focusing on structurally attractive market segments, where long-term growth drivers are less correlated with the broader economy, can deliver a more resilient portfolio.

Additionally, investing in domestic-focused companies lowers the susceptibility of dividends to foreign exchange volatility, which can be detrimental for UK investors seeking sterling-denominated income.

A focus on the fundamentals should be key in finding the businesses best equipped to deal with the crisis and highlight the benefits of sticking to an investment process.

It is vital to target profitable, higher margin cash generative businesses, with low or no gearing and strong balance sheets. In addition, high dividend and cashflow cover can help determine a company’s ability to continue trading without having to suspend or cut its dividend. Companies with a higher dividend cover can reinvest cashflow into future growth opportunities, thereby offering multi-year earnings growth as well as dividend growth potential.

As such, constant detailed analysis is important for ensuring understanding the ‘potential frailties’ of a holding.

Investors should look for managers that have actively engaged with management teams during the pandemic, rather than those who have sat back and watched.

The switch to conducting virtual meetings has been pretty seamless, with CEOs and CFOs available at relatively short notice. In fact, we have found meetings to be highly focused and sometimes more productive than face-to-face encounters.

These discussions serve to help us understand the difficulties that companies are facing on both a supply and demand front and what measures are available – such as renegotiating supply arrangements, imposing pay cuts or calling on government schemes. We need to have comfort that management are on the front foot and rapidly responding to protect and reposition the business in the new environment.

Investors should exercise greater caution during times of heightened volatility.

Having gone into the pandemic with higher capital reserves in the LF Gresham House UK Multi Cap Income Fund than usual, we have not rushed to deploy cash too quickly and have instead added money to higher conviction ideas. In companies where the dividend is secure and will be paid in the near term, committing further capital can lock in returns and contribute to annual income targets.

However, market sell-offs have also provided a timely opportunity to purchase bigger stakes in fundamentally sound businesses, particularly in the leisure industry.

Finally, with so much uncertainty in the market, investors shouldn’t be afraid of making tactical divestments to free up liquidity.

It is crucial to anticipate second order impacts beyond the imminent recession. Once economic activity resumes, certain business areas will take longer to recover. For this reason, we have cut holdings in more cyclically exposed companies, where the road to recovery will be lengthy. Investments in businesses that have not fallen enough, considering how much operations have been hit can be signal to move re-deploy those resources elsewhere. It is also important to anticipate second order impacts beyond the imminent recession.

Once economic activity resumes, certain business areas will take longer to recover. For this reason, we have cut holdings in more cyclically exposed companies, where the road to recovery will be lengthy.

The £64.9m* LF Gresham House UK Multi Cap Income Fund (formerly known as LF Livingbridge UK Multi Cap Income) invests primarily in small and mid-sized companies targeting an income with the potential for capital growth.

*As at 30 June 2020.

This article represents the opinions of the authors and should not be considered as investment advice.

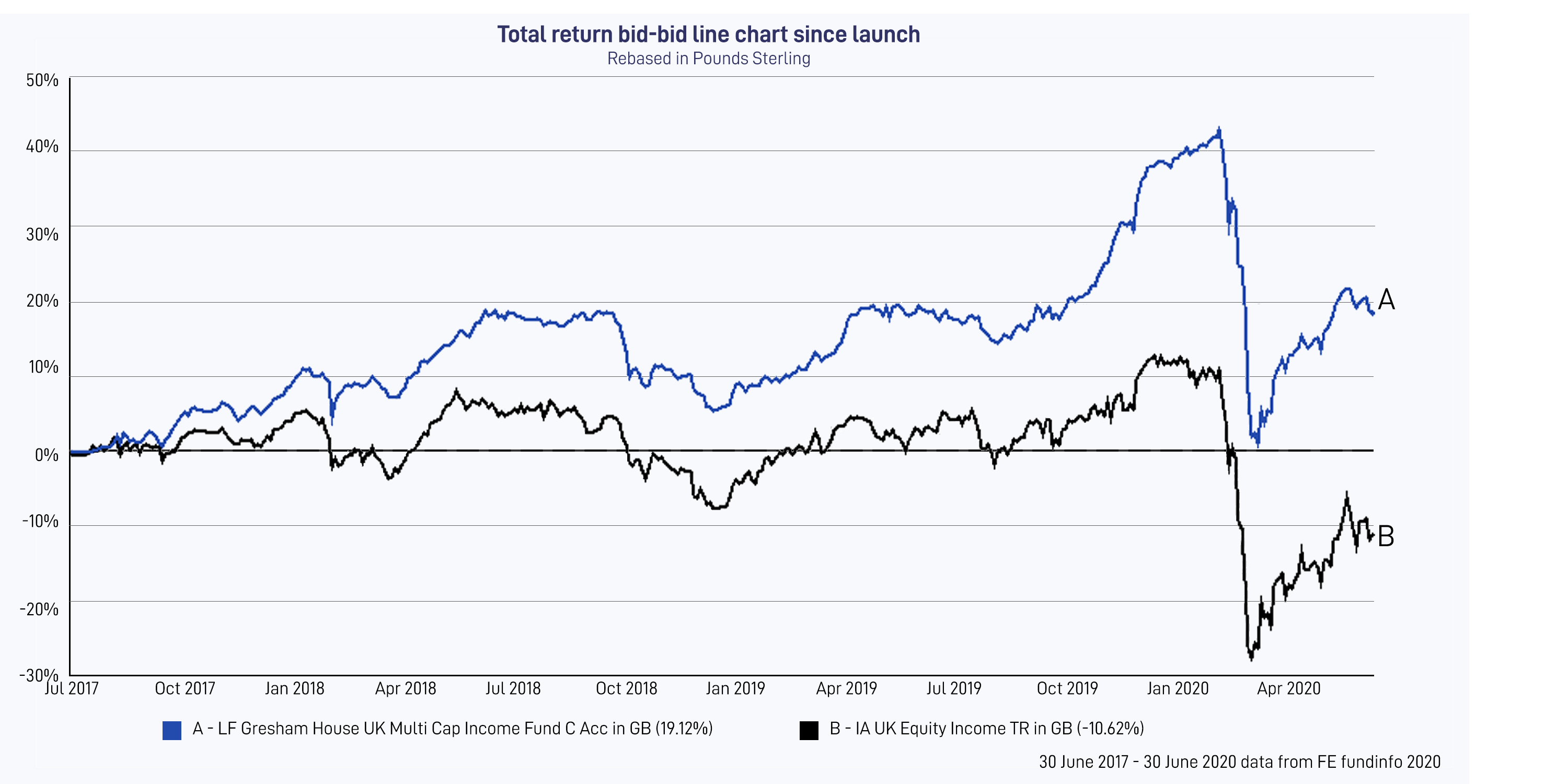

Performance of the Fund vs the IA UK Equity Income sector since launch

Since launch, the Fund has returned 19.12% against -10.62% for the IA UK Equity Income sector as at 30 June 2020.*

Past performance is not a reliable indicator of future performance. Your capital is at risk.