April 2025

April 2025

Monthly Monitor | April 2025

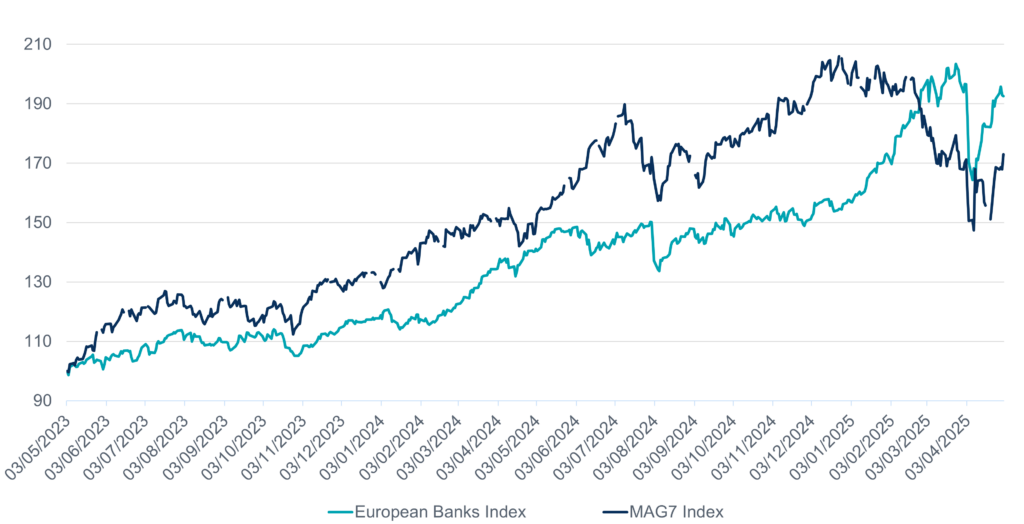

It may come as a surprise to many that the most unloved sector of the 2010’s (European Banks) has managed to outperform the ‘Magnificent Seven’ over the last two years. Despite the strong run of performance, valuations remain cheap and we believe earnings growth can continue to propel the share prices of European banks.

European banks vs Magnificent Seven

Source: Bloomberg, 3 May 2023 to 1 May 2025

From 2006 to 2020, European banks struggled because of the financial crisis, stricter regulation, and low interest rates. During this time, they were the weakest sector in terms of performance. It’s no surprise that many investors shunned them. However, since the COVID-19 pandemic, these European banks have started to recover, becoming more profitable and delivering performance. They’ve also returned record amounts of cash to shareholders. Still, the fact that their price-to-earnings (P/E) ratios haven’t improved suggests that investors are still unsure if this strong performance can last. European banks are also trading at a record discount to US banks and global financials.

Valuation on its own is not enough, the European banks are now a growth story. Investors spent the years post the financial crisis worrying about provisioning levels and capital ratios, the story is now about the income statement. The European Central Bank (ECB) rate cuts are now showing results. As of January, the total value of new loans given by banks to private companies and households over the past year reached 1.3% of GDP. That’s a big jump from just 0.2% a year earlier. This growth is happening in both household and business lending. The room for lending growth is considerable – household debt levels in Europe are back to low levels, last seen in the early 2000’s.

A sector with a long runway for growth, delivering value creating returns on tangible equity with strong balance sheets, while trading at very low valuations – what’s not to like?

Any views and opinions are those of the Fund Managers, this is not a personal recommendation and does not take into account whether any financial instrument referenced is suitable for any particular investor.

Capital at risk. If you invest in any Gresham House funds, you may lose some or all of the money you invest. The value of your investment may go down as well as up. This investment may be affected by changes in currency exchange rates. Past performance is not necessarily a guide to future performance.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or otherwise.

Want to keep up to date?

Subscribe using the form below to receive updates on our Monthly Monitor.