September 2025

September 2025

Monthly Monitor | September 2025

Headline global equity valuations are elevated, skewed by expensive US mega-caps. Beneath the surface, we see three compelling pockets of opportunity:

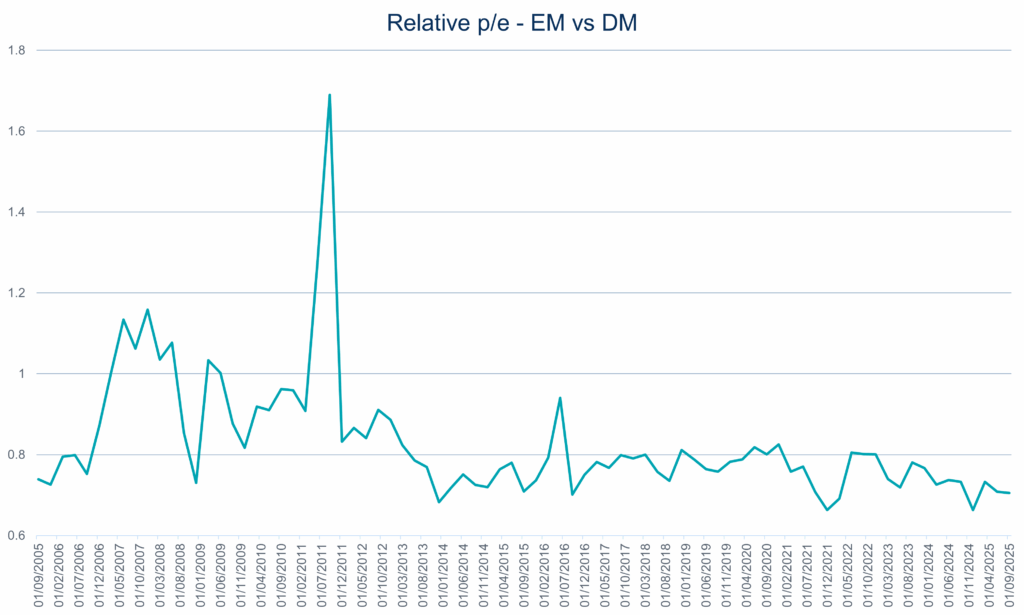

1) Emerging Markets (EM)

EM investing entails real risks, governance, Foreign Exchange volatility, and political instability, but the return potential and diversification benefits are significant.

Valuation and policy backdrop: EM equities are historically inexpensive, with several markets focused on governance improvements. A softer US Dollar further supports the set-up.

Consumption S-curve: Vietnam, India, Indonesia, and Nigeria’s combined population is c.2bn people, roughly double China’s population at the start of its 2000s boom. An estimated 600mn are entering the US$10–15k income band, when households typically add electricity, running water, and begin purchasing household appliances This coming demand inflection could rival, or even surpass, China’s 2000s consumption surge.

2) Developed Markets (DM) ex-US

Developed Markets outside the US are trading at levels consistent with attractive long-term returns and represent a substantial share of global GDP and market capitalisation.

- Potential catalysts to realise value include:

- Easing monetary policy

- Targeted fiscal support

- Ongoing structural reforms

- Lower relative budget deficits

- Lower starting valuations

- A weaker Dollar prompting rotation into non-US assets

Breadth is improving – we’re seeing attractive names hitting our screens across regions and industries, typically a favourable backdrop for active stock pickers.

3) Deep value in the US

The cheapest cohort of US equities is the only segment priced below its historical norms. By contrast, the most expensive cohort screens near the 85th percentile versus history, while the cheapest sits near the 6th percentile, highlighting a pronounced valuation spread and a fertile hunting ground for contrarian, value-oriented ideas.

Our response:

We maintain limited exposure to US corporates directly impacted by tariffs. We also complement equity positions with fixed income strategies to mitigate against a broader economic slowdown.

Derek Heffernan

Chief Investment Officer

Any views and opinions are those of the Fund Managers, this is not a personal recommendation and does not take into account whether any financial instrument referenced is suitable for any particular investor.

Capital at risk. If you invest in any Gresham House funds, you may lose some or all of the money you invest. The value of your investment may go down as well as up. This investment may be affected by changes in currency exchange rates. Past performance is not necessarily a guide to future performance.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or otherwise.

Want to keep up to date?

Subscribe using the form below to receive updates on our Monthly Monitor.