August 2025

August 2025

Monthly Monitor | August 2025

Global equity markets have rallied in recent weeks, but beneath the surface important risks remain. President Trump’s decision to step back from his initial tariff proposals has helped fuel optimism. Yet, as John F. Kennedy once reminded us, “The time to repair the roof is when the sun is shining”.

With that in mind, we explore the key risks that could undermine the current mood, and how we are positioning in response.

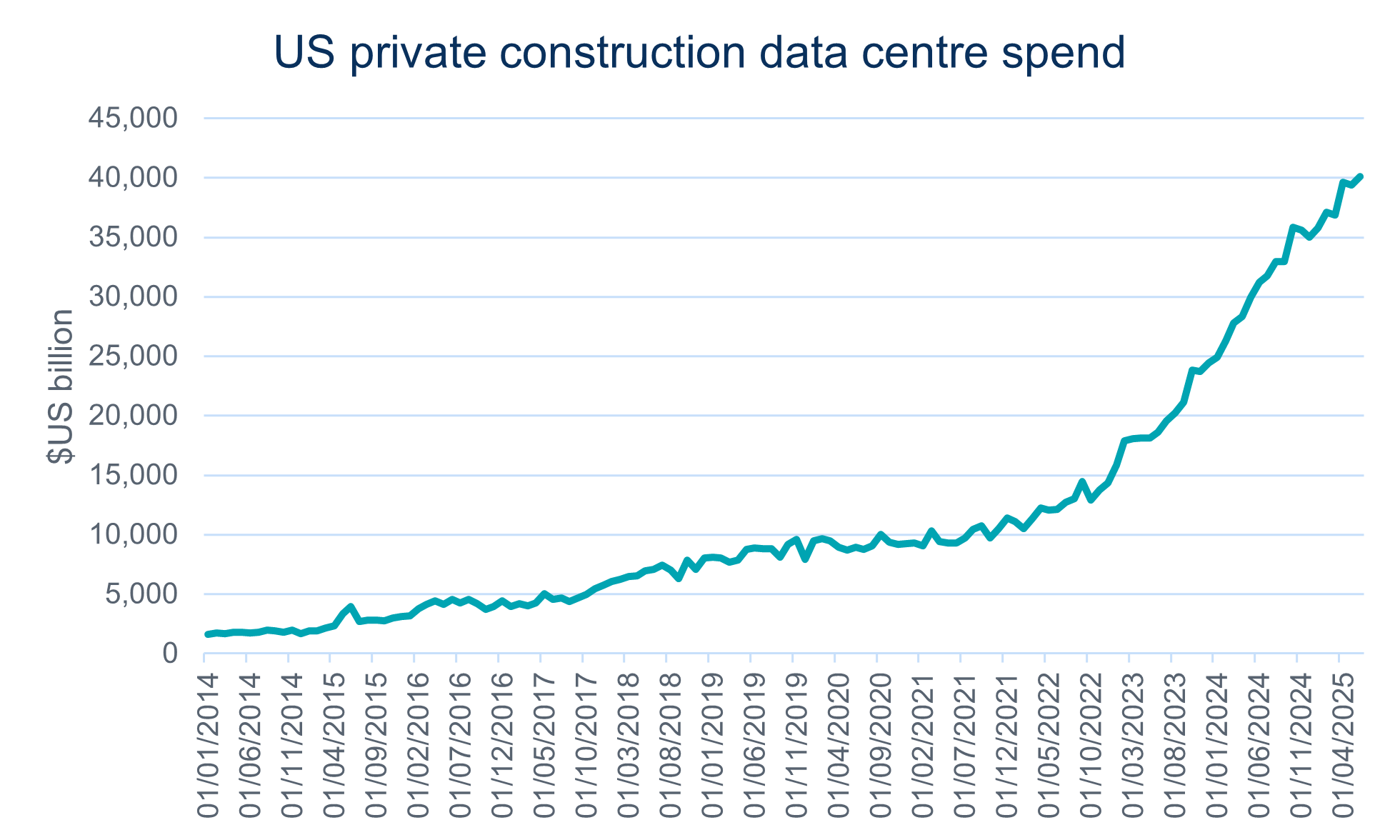

Risk 1: AI – hyper investment by hyperscalers

The AI arms race among hyperscalers is accelerating, with more than $400bn expected to be invested this year. Whether this extraordinary capital deployment will generate sustainable returns remains an open question.

This boom is self-reinforcing in practice. For example, if Amazon spends $1bn on Nvidia chips, Nvidia records around $500mn in profit, while Amazon books only a $150mn depreciation charge. The result is an apparent $350mn uplift in aggregate earnings for the Magnificent Seven.

Hyperscalers cannot afford to stand still given the existential threat of disruption. Yet investors will eventually demand evidence of real returns. If these fail to materialise, the earnings outlook for the Magnificent Seven, and by extension the broader index, could deteriorate sharply. The wider economic impact would also be significant, with data centre construction having been a major contributor to GDP growth.

Our response:

We are avoiding direct exposure to hyperscalers and data centres. Predicting winners in this arms race is highly uncertain, and the dynamics have shifted. The original appeal of the Magnificent Seven was their ability to compound earnings without heavy capital expenditure, often under monopoly-like conditions. That advantage is no longer present. Instead, they are moving into a more competitive and costly arena with lower barriers to entry.

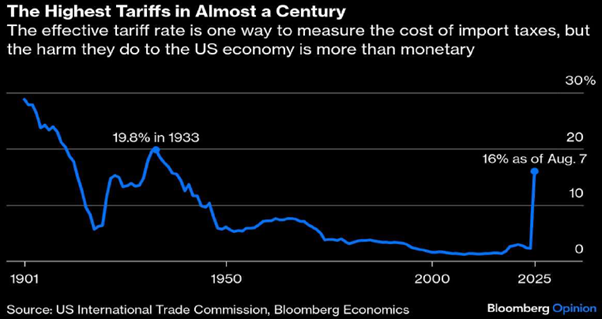

Risk 2: Tariffs

Despite recent watered-down announcements, tariffs remain a pressing risk. Initially, consumers front-loaded purchases and corporates built up inventories to cushion the impact. As these buffers decline, however, the effects will begin to bite more acutely.

The scale of the challenge is striking. We have not seen tariff levels of this magnitude in more than 75 years.

The US imports goods worth over $4 trillion annually. A 14% increase in tariffs equates to roughly $560bn in additional costs, around 2% of GDP. These costs ultimately fall on companies through margin compression, and on consumers through weaker purchasing power.

Our response:

We maintain limited exposure to US corporates directly impacted by tariffs. We also complement equity positions with fixed income strategies to mitigate against a broader economic slowdown.

Reasons for optimism

Even so, there are also compelling reasons for optimism. Several factors continue to support equities:

- Attractive valuations outside the US

- Loose fiscal policy across the US, Europe and increasingly China

- Low oil prices, providing a tailwind for consumers and corporates

- Ample liquidity, sustaining demand for risk assets

Conclusion

Balancing these risks and opportunities is key for investors. The AI investment cycle and tariffs present real challenges to earnings and economic growth. However, with supportive fiscal conditions, benign energy markets, and reasonable valuations beyond the US, we believe investors can continue to generate attractive through-the-cycle returns.

We will continue to monitor these dynamics closely and adapt positioning to help clients navigate an uncertain but opportunity-rich environment.

Derek Heffernan

Chief Investment Officer

Any views and opinions are those of the Fund Managers, this is not a personal recommendation and does not take into account whether any financial instrument referenced is suitable for any particular investor.

Capital at risk. If you invest in any Gresham House funds, you may lose some or all of the money you invest. The value of your investment may go down as well as up. This investment may be affected by changes in currency exchange rates. Past performance is not necessarily a guide to future performance.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or otherwise.

Want to keep up to date?

Subscribe using the form below to receive updates on our Monthly Monitor.