Monthly Monitor | April 2026

Emerging markets: Rotation, not a rally

Monthly Monitor: Emerging Markets: Rotation, not a rally

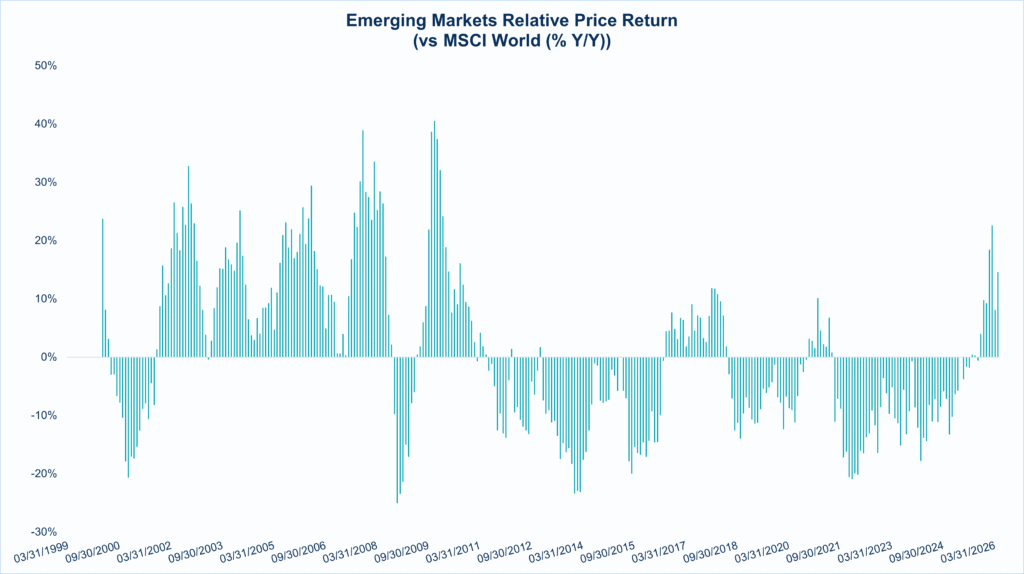

Emerging Markets (EM) have quietly reasserted themselves.

Following the drawdown triggered by the escalation of conflict in the Middle East, EM equities have recovered strongly, with the MSCI Emerging Markets Index now approaching prior highs. While this resilience may appear surprising given geopolitical and energy sensitivities, it is important to recognise how difficult this asset class has been historically.

After declining c. 23% between 2008 and the end of 2022 (c. -2% annualised), the MSCI Emerging Markets Index has since risen nearly 70%, or c. 17% annualised. Even more striking, only c. 30% of months since January 2009 have delivered a positive return, highlighting just how inconsistent EM performance has been over the past nearly two decades.

Against that backdrop, the key question is why EM is now performing so strongly. Our view is that this is not a tactical rebound, but the early stages of a more durable rotation, supported by improving earnings momentum, resilient macro conditions and still undemanding valuations.

Source: Bloomberg 31 January 1999 to 31 January 2026

The structural case remains intact

The long-term case for emerging markets is well understood but remains underappreciated in asset allocation.

Demographics and rising incomes continue to drive a structural shift in consumption. As economies move through the $10,000-$20,000 income band, spending transitions from basic necessities towards discretionary and branded goods, reinforced by a growing wealth effect. This is increasingly supported by stronger household balance sheets and deeper domestic demand.

Importantly, market structure has also evolved. The marginal buyer of EM assets is now increasingly domestic rather than foreign, with local savings pools and pension systems providing a more stable source of capital and reducing vulnerability to external shocks.

Why now? Earnings, resilience and valuation

The key question is timing, and here the backdrop has clearly improved.

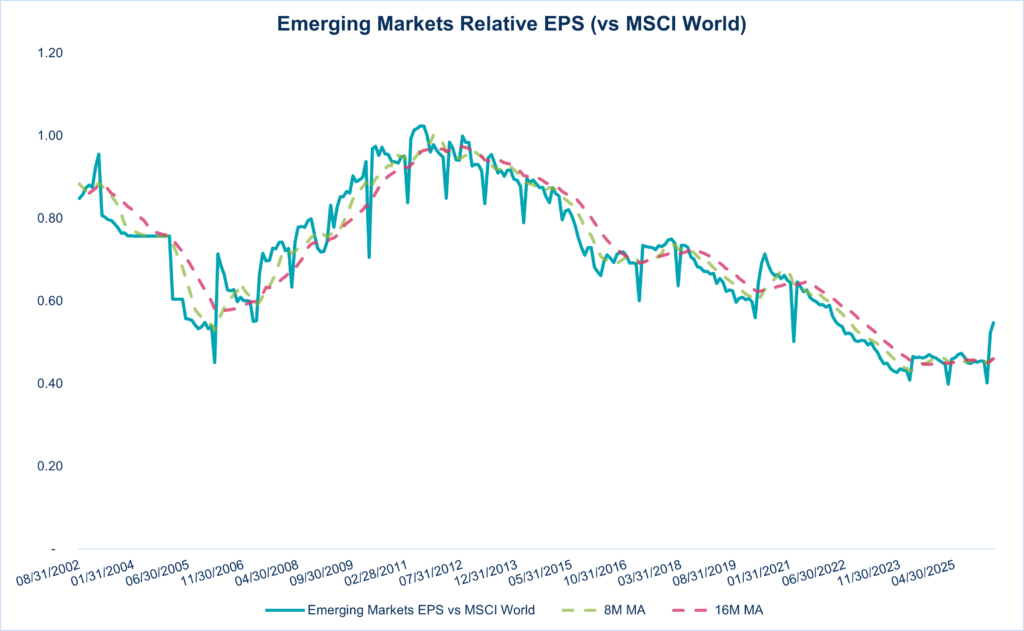

- First, earnings momentum has turned

After a prolonged period of downgrades, forward earnings are stabilising and improving, and have proven resilient through the recent energy shock, in contrast to prior episodes such as 2022.

Source: Bloomberg 31 August 2001 to 31 December 2025

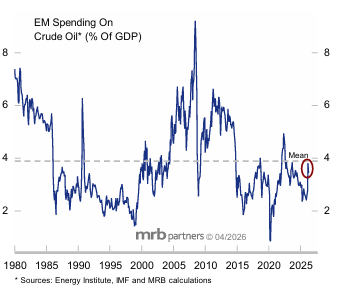

- Second, the macro environment remains supportive

Oil expenditure as a share of GDP remains manageable, while growth indicators are improving following an extended period of weakness. Monetary and fiscal policy also remain broadly accommodative.

EM spending on Crude Oil* (% of GDP)

*Sources: Energy Institute, IMF and MRB calculations

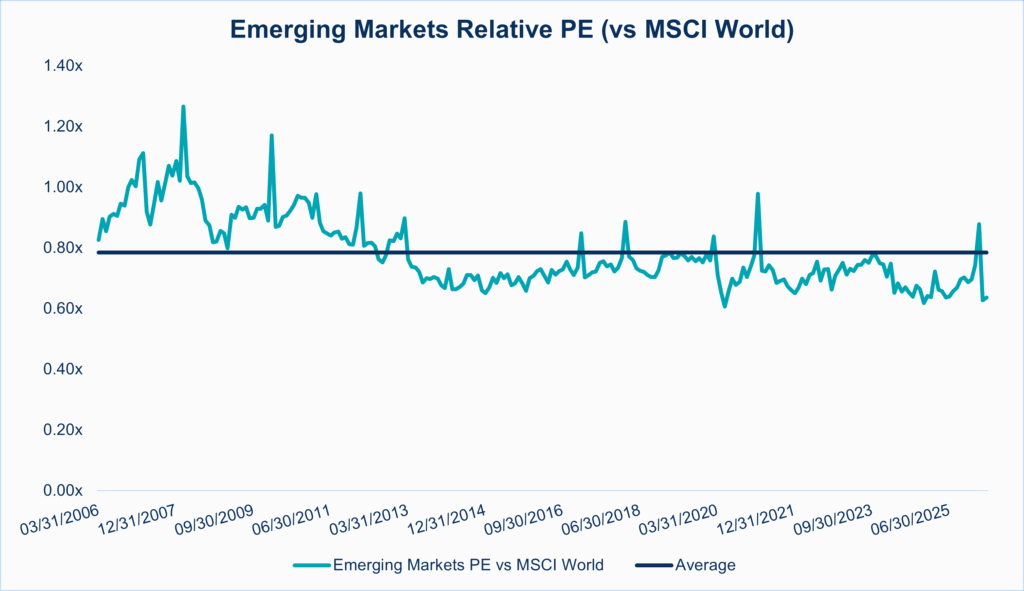

- Third, valuations remain compelling

EM equities continue to trade at a c. 35% discount to developed markets, a level that appears inconsistent with the improving earnings trajectory. Recent volatility has also reset valuations, providing a more attractive entry point.

Source: Bloomberg 31 March 2006 to 31 January 2026

The role of the US Dollar and capital flows

One of the more underappreciated drivers of EM performance is the direction of the US Dollar. In previous Monitors we noted that we were structurally short the USD, and that thesis largely played out last year, with the Dollar Index (which compares the USD to a basket of currencies) falling by c. 10% last year and had declined a further 1% by the end of February this year prior to the breakout of conflict in the Middle East.

A weaker US Dollar remains a key tailwind. It eases financial conditions, supports EM currencies and enhances USD earnings. While geopolitical tensions have temporarily interrupted this trend, the broader setup remains conducive to Dollar weakness.

At the same time, capital flows are beginning to diversify away from the US. Elevated valuations and rising policy uncertainty are encouraging a rotation into markets with lower starting valuations and improving fundamentals, a dynamic that should benefit EM.

A different asset class than before

It is also important to recognise that “emerging markets” today are fundamentally different from the asset class that underperformed over the past decade.

Historically, EM performance was highly dependent on external capital and global liquidity conditions. Today, deeper domestic capital markets, stronger policy frameworks and more balanced growth models have reduced this dependence. The result is an asset class that is less fragile and more capable of sustaining periods of outperformance.

Risks: Energy and geopolitics remain key

The key risk remains energy. A sustained disruption leading to materially higher oil prices would challenge growth and pressure risk assets. Geopolitical tensions and trade frictions may also lead to intermittent volatility.

Conclusion: The rally has room to run

After more than a decade of underperformance, emerging markets are benefiting from a more favourable alignment of fundamentals. Earnings are improving, the macro backdrop is resilient and valuations remain attractive.

While volatility is likely to persist, we believe this represents the early stages of a broader rotation rather than a short-term rally. For valuation-driven investors, emerging markets remain one of the more compelling opportunities in global equities.

Callum Heapes Patrick Lawless

Investment Analyst Investment Committee Chair

Any views and opinions are those of the Fund Managers, this is not a personal recommendation and does not take into account whether any financial instrument referenced is suitable for any particular investor.

Capital at risk. If you invest in any Gresham House funds, you may lose some or all of the money you invest. The value of your investment may go down as well as up. This investment may be affected by changes in currency exchange rates. Past performance is not necessarily a guide to future performance.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or otherwise.

Want to keep up to date?

Subscribe using the form below to receive updates on our Monthly Monitor.