January 2025

January 2025

2024 was a relatively disappointing year for most valuation conscious investors. Assets including equities and bonds re-entered ‘bubble’ like territories, and the fourth quarter in particular saw speculative assets regain the limelight. We are in a period that is reminiscent of 2021, the dotcom bubble, and the Nifty 50 or one decision stocks of the 1970s.

A few examples of the current ‘American exceptionalism’ narrative in 2024 include:

- Tesla adding over $800bn in market capitalisation (more than the market capitalisation of the next ten automakers combined) between 23 October and the end of 2024, despite reporting their first drop in annual sales

- The market capitalisation of the crypto currency universe doubling

- US value stocks falling for 14 consecutive days in December, while US ‘glamour’ stocks hit new highs, a level of underperformance only seen in the Dotcom bubble

- Europe being completely ignored by investors – only two of the top ten European companies delivered positive returns, while in the US all of the top ten companies delivered double, or triple-digit returns. The largest 15 companies in the US now account for the same market capitalisation as Japan, Europe and emerging markets

- The divergence between large cap and small cap at levels never witnessed before. Small market capitalisation stocks have been completely ignored – including even technology stocks. US small cap tech index fell 1% in 2024

As a result of the above, the US is now effectively the global index and valuations are likely to condemn global equity indices to mediocre long-term returns.

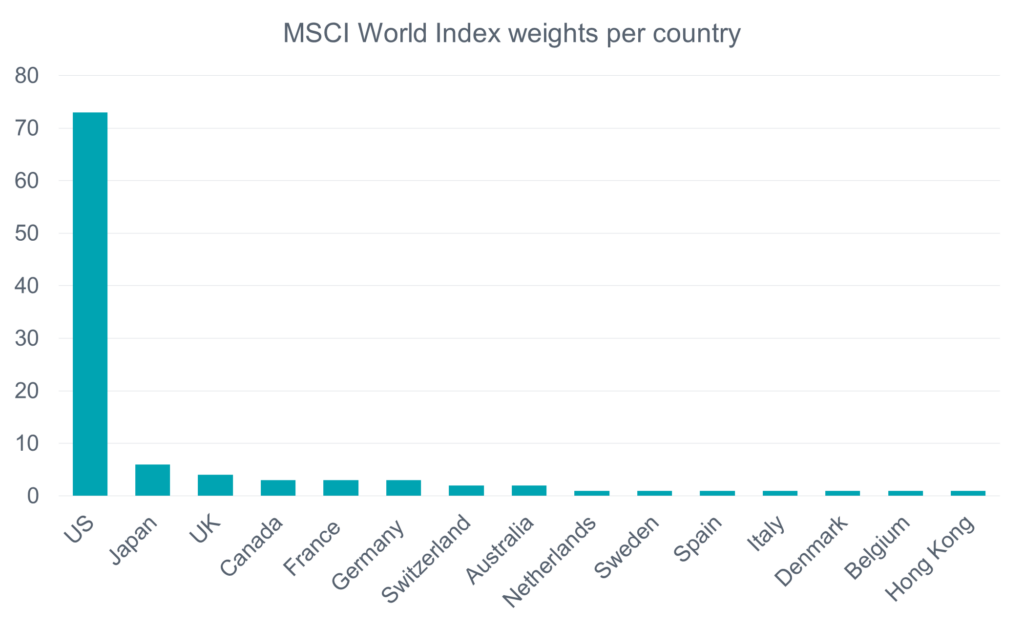

The US has 4% of the world’s population, 25% of global GDP, and 33% of global profits. However, given the excessive valuations of US companies, it now accounts for 73% of the MSCI World Index.

Source: Gresham House Ireland Investment Management

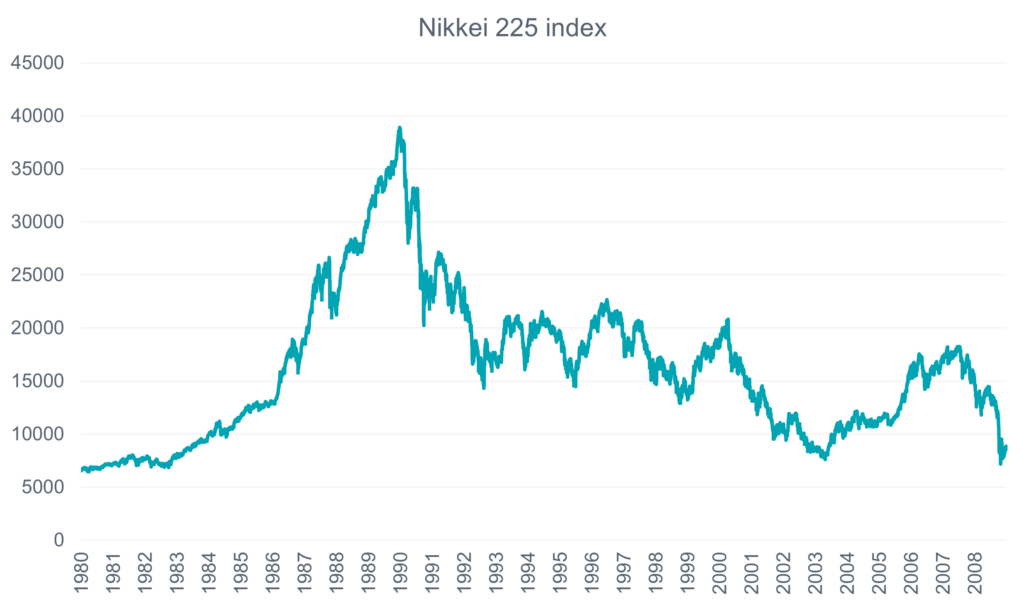

The only similar period of dominance in recent history is Japan’s superior position in consumer technologies in the 1980s. The country made up 15% of world stock market capitalisation in 1980, and by 1989 it represented 45% of the global equity markets. At the time, Japanese share prices increased three times faster than corporate earnings, echoes of which are currently being seen in US markets.

After reaching nearly 39,000 in December 1989, the Nikkei lost over 80% of its value over the next eighteen years.

Source: Gresham House Ireland Investment Management, Bloomberg

While the valuations in the US today are not as extreme as we saw in Japan in the 1980s, they are still at levels where future returns have been weak. In our view, mega cap US equities are over valued, over owned and over hyped which we believe increases the risk.

The US market has some of the best companies in the world, however paying a sky-high multiple for those companies compared to the rest of the world matters more than their inherent quality. It is difficult to time the end of the bubble, but one thing we do know is that all bubbles end and this one will be no different.

When the Dotcom bubble burst, value investing delivered strong positive returns:

Source: Gresham House Ireland Investment Management

Conclusion

We have always taken the big risks off the table, for example:

- Did not hold Irish property in 2006

- Did not hold European banks in 2007

- Held limited European exposure during the 2011 Sovereign Debt Crisis

- Held no fixed income when the bond bubble burst in 2022

- We do not invest in areas with large valuation risk

We are finding plenty of pockets of value outside the US mega cap space, in particular we believe the UK and continental Europe hold attractive opportunities and therefore this is where we are focusing our research efforts.

Looking foolish in the short term is the price to be paid to in order to protect capital and not take valuation risk. We remain comfortable that over the full cycle our funds will deliver superior returns compared to the broad indices while taking on significantly lower levels of risk.

Any views and opinions are those of the Fund Managers, this is not a personal recommendation and does not take into account whether any financial instrument referenced is suitable for any particular investor.

Capital at risk. If you invest in any Gresham House funds, you may lose some or all of the money you invest. The value of your investment may go down as well as up. This investment may be affected by changes in currency exchange rates. Past performance is not necessarily a guide to future performance.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or otherwise.