Monthly Monitor | January 2026

Precious Metals: Valuation and Tactical Rotation

We have had exposure to gold through ETF holdings in our multi-asset portfolio for many years despite not being “gold bugs” by any means. Our logic for holding gold was based on economic history. We view gold as insurance and as a store of value when confidence in fiat currencies and financial engineering wavers or collapses.

Policy interventions that create stability, such as financial repression, ultimately create more fragility that can destroy confidence in nominal assets. Gold is one of the few assets that doesn’t embed long-term credit risks.

The long-run insurance view we had on gold is supplemented by medium-term dynamics that we believed would drive the price higher, namely that gold is in a structural bull market driven by reflationary policy, a weakening US Dollar and demand from non-traditional buyers.

- Global reflation: Fiscal and monetary regimes globally are more expansionary than they have been in decades, which increases the risk of currency depreciation

- Scarcity & demand dynamics: Supply is relatively inelastic. Mining capacity remains constrained after years of underinvestment while demand drivers include central bank buying and institutional position accumulation

- US Dollar Bear trend: A secular bear US Dollar supports commodities and precious metals as alternative stores of value and liquidity reserves

Essentially, we hold gold to protect against systemic fragility and because of the irresponsible reflationary policy regime we are faced with.

Valuing gold is very difficult given the lack of cash flows. We tend to look at cross-asset relative valuations and price moves. The chart below shows the move in gold price relative to the 10-year US Treasury. This clearly shows that gold has become the most effective asset to hedge equity risk.

Chart 1: Gold vs 10-year US Treasury

Source: Bloomberg. Data from 5 March 1995 – 28 January 2026

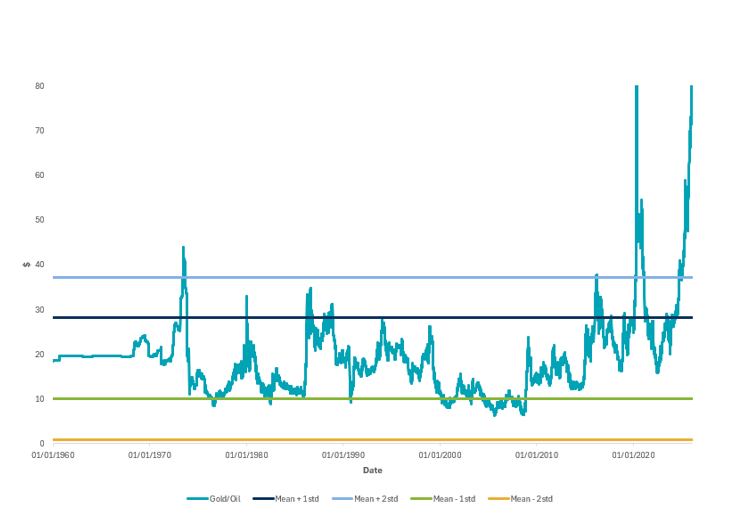

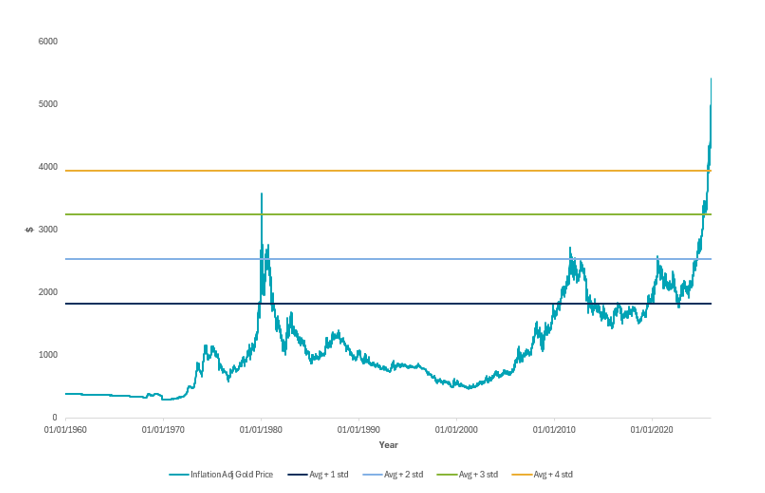

There is no doubt gold has become expensive relative to other asset classes, money supply and in real terms.

Chart 2: Gold versus Oil

Source: Bloomberg. Data from 1 January 1960 – 12 February 2026

Chart 3: Gold in real terms

Source: Bloomberg. Data from 1 January 1960 – 12 February 2026

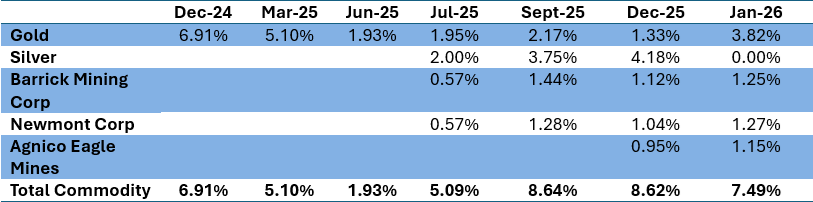

Multi Asset Commodity exposures (Added to Silver on 7 July 2025; exited on 28 January 2026)

Regarding our exposure to gold and precious metals, we have traded tactically around the price divergence between the precious metal prices and the miners.

Over the summer, we saw a significant divergence between gold, which had rallied strongly, and silver, which had lagged (see chart 4 below). We also saw a divergence between gold and the valuation of gold miners. We used the divergence as an opportunity to take positions in silver and gold miners.

Chart 4: Gold/Silver ratio

Source: Bloomberg. Data from 1 January 1960 – 12 February 2026

After the explosive rally in the price of silver, we sold our silver exposure on 28 January 2026. We could no longer support the investment on fundamental grounds. We have maintained our position in both gold and gold miners and believe they will produce strong numbers for the coming year.

Gresham House Global Multi Asset Fund Precious metals portfolio allocation:

Source: Gresham House Ireland Investment Management

Outlook and conclusion:

We continue to maintain our position in gold but have migrated towards the miners as we believe that is where the value lies. After the impressive rally, we are monitoring technicals closely and will take further actions to reduce our positions should valuations become more stretched.

Derek Heffernan

Chief Investment Officer

Any views and opinions are those of the Fund Managers, this is not a personal recommendation and does not take into account whether any financial instrument referenced is suitable for any particular investor.

Capital at risk. If you invest in any Gresham House funds, you may lose some or all of the money you invest. The value of your investment may go down as well as up. This investment may be affected by changes in currency exchange rates. Past performance is not necessarily a guide to future performance.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or otherwise.

Want to keep up to date?

Subscribe using the form below to receive updates on our Monthly Monitor.